in India – Things to Know!")

Banks and financial institutions worldwide are primarily responsible for a variety of financial transactions, including deposits and loans. In the current scenario, financial companies other than banks have emerged to meet the growing needs and demands of people in the digital age. Non-bank financial companies (NBFCs) are one of the types of financial companies that offer strong competition to banks in certain areas.

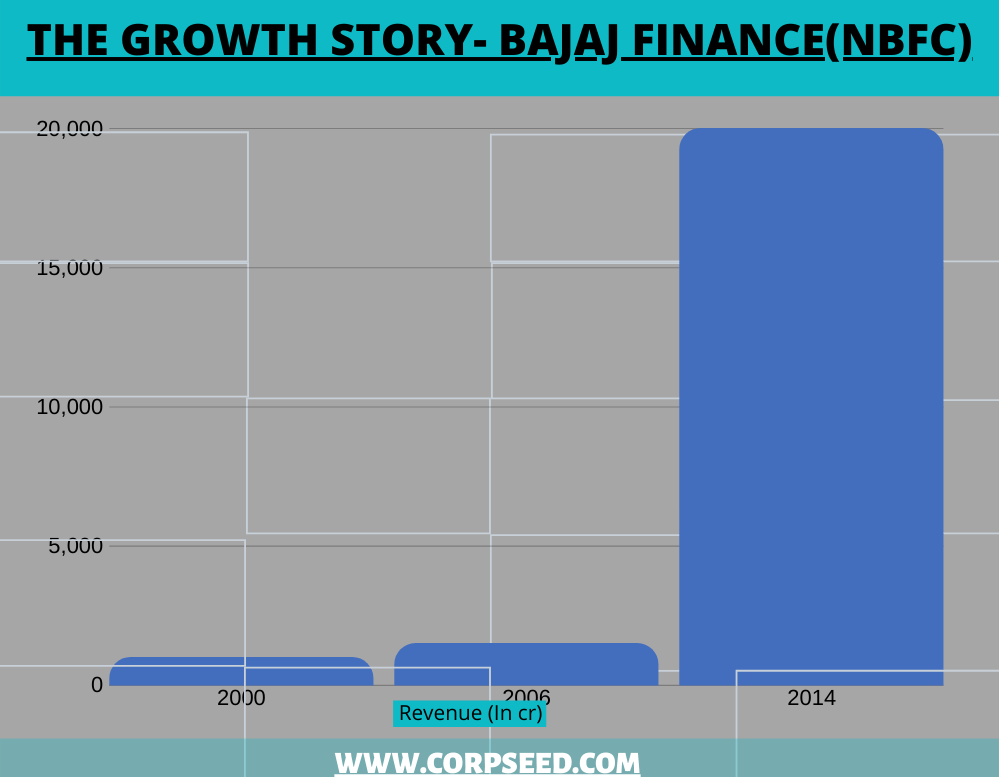

A popular example of NBFC in India is Bajaj Finance, which was established in 1987 and has been a huge success ever since. Here is a chart that shows sales growth over the years.

In general, a Non-Banking Financial Company (NBFC) can be defined as a publicly listed company under the Companies Act of 1956, which is responsible for loans and advances, stock/debit purchases, etc. Financing by chit, etc. is responsible, etc. However, it is not connected to companies active in agriculture, industry, or the sale/purchase of goods and assets.

NBFC types

1. Loan company (LC)

LCs are responsible for making advances and loans for commercial or other purposes.

2. Asset Finance Company (AFC)

The AFC is responsible for increasing the financing of physical assets such as automobiles, earthmoving machinery, etc.

3. Investment company (IC)

The investment company is responsible for the purchase of securities such as stocks, debts, stocks, etc.

4. Infrastructure financing company (IFC)

IFC must meet a long list of criteria, some of which include:

At least 75% of total assets for infrastructure loans.

75% CRAR

Net funds of at least £ 300 million.

The “A” credit rating.

5. Mortgage Guarantee Company (MGC)

MGCs are those that depend on 90% of the mortgage guarantee income and have a net fund of £ 100 million.

6. NBFC – Non-Operating Holding Finance Company (NBFC-NOFHC)

NBFC-NOFHC is a newly established developer bank that owns banking and financial services and is regulated by the RBI.

Other NBFCs of this type now operate successfully in the Indian banking and financial services market. Each has an individual role to play and responds to the individual needs of their clients.

Who regulates non-bank financial companies?

Unlike banks, not all NBFCs are regulated by the Reserve Bank of India (RBI). Most NBFCs are regulated by other authorities based on factors such as their net worth, type of business, etc. Here is a list of some NBFCs and their regulators in the Indian context …

Venture capital funds, Commercial banking, regulated by SEBI

Part of state government funds

Housing financing from the National Housing Bank (NHB)

Nidhi Company, run by the Ministry of Business Affairs

How are NBFCs different from banks?

There are some differences between the way banks and NBFCs operate. The most basic are:

The RBFC is not authorized by the RBI to implement payment and settlement systems (NEFT, RTGS, debit/credit cards) in India.

You cannot write checks or accept demand deposits.

Unlike banks where deposits of up to 1 lake are insured with the Deposit Protection and Credit Guarantee Corporation (DICGC), deposits with the NBFC do not have such guarantees and guarantees.

conclusion

The NBFC market is growing in India and has tremendous development potential in the face of the financial technology revolution and technological advancements in AI and machine learning (ML). If you are looking for banking solutions that can help your NBFC reach new financial milestones, contact our experts today.